All that Glitters is Not Gold

By: John S. Weitzer, CFA

Sep 21, 2018 | 3 min. read

The title for this short commentary comes from William Shakespeare’s play, The Merchant of Venice. The exact line is: “All that glitters is not gold—often have you heard that told.” [1] To be clear upfront, this commentary is not about gold or any other precious metal, for that matter. Instead, I want to highlight an investment risk I see growing in the U.S. corporate bond market.

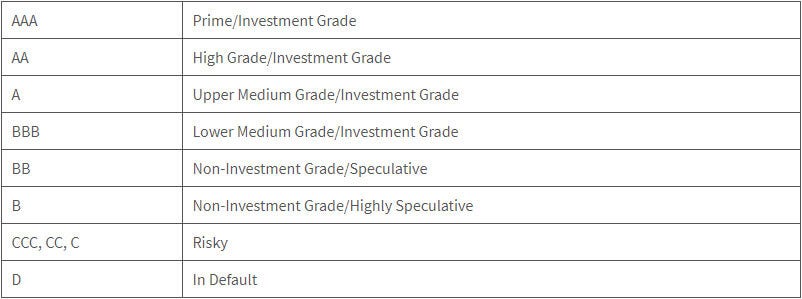

Before discussing that risk, however, a brief explanation of how the quality of bonds is determined and expressed may be helpful. Generally, bonds are rated on a scale ranging from AAA (like a U.S. Treasury bond) to D (as in “the bond is in default”). The credit rating of a bond is an indicator of the creditworthiness or capacity to pay of the company that issued the bond. The table below shows the full spectrum of ratings.

The rising risk that I see in the U.S. corporate bond market (defined as bonds issued by U.S. corporations and not government entities) resides in the BBB rating category, which contains the lowest rated investment grade bonds. A BBB rating indicates that the issuing company has adequate capacity to meet its financial commitments, but that adverse economic conditions or changing circumstances may weaken its capacity to meet its financial commitments.[2]

So, what is going on with BBB bonds from U.S. companies? For starters, the size of the BBB bond market has exploded in the last decade.[3] Triple-B bonds now represent over 50 percent of the total investment grade corporate bond market in the U.S ($3 Trillion of $6 Trillion). That’s up from $700 billion in 2008, when they made up less than a third of the market.[4] However, a larger BBB bond market does not necessarily translate to a riskier BBB bond market. It’s the high degree of leverage – or debt relative to earnings – in the BBB bond market that is a greater concern to me. The average ratio of debt to a company’s true earnings[5] for corporate credits is now at an all-time high: 3.2 times versus 2.1 times in 2007.[6] This would be equivalent to having a job that paid you $50,000 a year and having $160,000 of personal debt. But that is only the average. According to Barron’s, 37 percent of BBB corporate credits have debt-to-earnings ratios in excess of five times (or $250,000 of debt compared to a $50,000 salary in our example).[7] Dan Fuss, a highly respected fixed-income portfolio manager for over 60 years, estimated that if BBB credits were classified solely on leverage (debt relative to earnings) and not on other factors, such as cash flow, 28 percent of the investment grade credit index would be considered junk or high-yield bonds.[8] Some BBB corporate bonds, even though rated as investment grade, may be closer in nature and risk to BB bonds, which are speculative. Indeed, all that glitters is not gold.

All of this is very interesting, but as a close friend would say, what does that have to do with the price of tea in China? Here is the connection: Within Asset Management Solutions (AMS), we do not use passive – or indexed – bond funds. This means that, unlike many managed portfolio programs, bond indices do not dictate what bonds we hold in our portfolios. Instead, we rely on active bond-fund managers who perform credit research on each company’s debt issues. They are empowered to be more selective than index funds and that is how we prefer it.

Many of the bond-fund managers that we work with have voiced concerns over the increase in debt at the bottom end of the investment-grade universe (where those BBB corporate bonds reside), and they are guarding against this increased risk. We have hired these experienced professionals to carefully sift through all of the bonds that glitter in order to avoid the “fool’s gold” represented by those higher-risk BBB issues – and, by consequence, to lower the credit risk to which your portfolio is exposed. It’s just one more way we seek to manage the investment risks within your AMS portfolio.

- The Merchant of Venice by William Shakespeare, Act II, Scene VII (circa 1596-1599). In the actual quote, the Old English word “glister” is used instead of “glitter.”

- https://www.bankersalmanac.com/addcon/infobank/credit_ratings/standardandpoors.aspx.

- Where the Bond Market’s Next Big Problem Could Start, by Vito J. Racanelli, Barron’s (August 17, 2018).

- Where the Bond Market’s Next Big Problem Could Start, by Vito J. Racanelli, Barron’s (August 17, 2018).

- As measured by “Earnings before Interest, Taxes, Depreciation and Amortization or EBITDA. EBITDA is one indicator of a company’s financial performance and is used as a proxy for the true earnings potential of a business. Investopedia – EBITDA (https://www.investopedia.com/terms/e/ebitda.asp).

- Where the Bond Market’s Next Big Problem Could Start, by Vito J. Racanelli, Barron’s (August 17, 2018).

- Where the Bond Market’s Next Big Problem Could Start, by Vito J. Racanelli, Barron’s (August 17, 2018).

- Where the Bond Market’s Next Big Problem Could Start, by Vito J. Racanelli, Barron’s (August 17, 2018).

The information in this report was prepared by John Weitzer, Chief Investment Officer of First Command. Opinions represent First Command’s opinion as of the date of this report and are for general informational purposes only and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally. First Command does not undertake to advise you of any change in its opinions or the information contained in this report. This report is not intended to be a client-specific suitability analysis or recommendation, an offer to participate in any investment, or a recommendation to buy, hold or sell securities. Do not use this report as the sole basis for investment decisions. Do not select an asset class or investment product based on performance alone. Consider all relevant information, including your existing portfolio, investment objectives, risk tolerance, liquidity needs and investment time horizon. Should you require investment advice, please consult with your financial advisor. Risk is inherent in the market. Past performance does not guarantee future results. Your investment may be worth more or less than its original cost. Your investment returns will be affected by investment expenses, fees, taxes and other costs.

All estimates provided are for informational purposes only and should not be relied on to make investment or other decisions. Should you require investment advice, please consult with your financial advisor. Risk is inherent in the market. Past performance does not guarantee future results. Your investment may be worth more or less than its original cost. Your investment returns will be affected by investment expenses, fees, taxes and other costs.

The S&P 500 Index is widely regarded as the best single gauge of the U.S. equities market. This world-renowned index includes a representative sample of 500 leading companies in leading industries of the U.S. economy. Although the S&P 500 Index focuses on the large-cap segment of the market, with approximately 75% coverage of U.S. equities, it is also an ideal proxy for the total market. An investor cannot invest directly in an index.

Get Squared Away®

Let’s start with your financial plan.

Answer just a few simple questions and — If we determine that you can benefit from working with us — we’ll put you in touch with a First Command Advisor to create your personalized financial plan. There’s no obligation, and no cost for active duty military service members and their immediate families.