Worth Its Weight In Gold?

By: Matt Wiley, CFA

Director, Investment Management

Sep 18, 2020 | 5 min. read

Gold has been on an impressive run lately, but it hasn’t proven to be an investment for all seasons.

2020 has been a difficult year for investors to navigate: Stock markets have been volatile, bonds yields have declined significantly, the political landscape is daunting, and the U.S. is issuing new debt at a historic pace to combat the COVID-related economic slowdown. In such an environment, it’s understandable that alternatives to traditional asset classes and hedges are gaining attention, and one of those that is making the rounds through infomercials again is gold.

Indeed, the timeless relic has had one heck of a run this year, rising roughly 30 percent as of the end of July and breaching the $2,000/troy ounce threshold for the first time in history. But year-to-date momentum aside, gold enthusiasts – despite having hibernated for most of the last decade – will argue that the yellow metal deserves a place in any efficient portfolio, serving as the perfect insurance policy regardless of current economic conditions, for the following reasons:

- Inflation: Most often associated with either a roaring economy, or more recently, a wave of global fiscal and monetary largesse, rising inflation expectations would be expected to precede a loss in purchasing power. In this light, gold is considered a viable store of currency.

- Deflation: If the economy cracks or the money supply contracts, assets rotate into safe havens, which gold has long been widely considered to be.

In theory, it’s a no brainer. In practice, however, the record is not so shiny. Consider this:

- “If you strip out the 1970s, you find the relationship between gold and inflation is quite weak.”[i] In fact, according to monthly data sourced from Bloomberg, the correlation between gold and the Consumer Price Index (i.e. inflation) since 1980 is essentially zero.

- As for the safe haven trade, “looking back at all 15% or worse S&P 500 drawdowns from 1975 through today – times when investors could reasonably feel like stocks were in crisis territory – gold has only ‘worked‘ about half the time.”[ii]

That being said, there is one asset that shows a fairly consistent relationship against gold, and that is the U.S. dollar. Using the Bloomberg US Dollar Index as a proxy since its inception on 12/31/2004[iii], for example, gold has exhibited a roughly -0.5 monthly correlation against the buck. So, while less effective against inflation in general, gold seems to be an effective hedge against weakness in the greenback, which clearly has implications toward preservation of purchasing power as well.

But before you run out to hedge your currency risk with Krugerrands, note that the S&P 500 Index during this same period has actually produced almost exactly the same negative monthly correlation to the U.S. dollar as gold! Accordingly, simply owning stocks has proven an effective hedge for the foreign exchange markets as well. So, which is the better hedge? Consider the following:[iv]

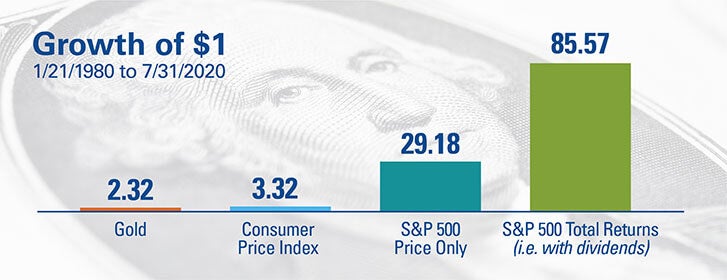

- At the peak of the Carter-era global inflation panic, gold traded briefly to $850 on January 21, 1980. Thus, it has basically returned 2.3 times its initial investment over the last 40 years, even after 2020’s stellar run.

- The Consumer Price Index over that same timeframe rose about 3.3 times.

- The S&P 500, on the other hand, was 112 on January 21, 1980. As of July 31, 2020, it was about 3271, almost 30 times its original investment. And that is before you include the dividends, which brings us to our next point…

- Gold does not produce any income. Stocks, on the other hand, do. Most stocks pay dividends, and they comprise a significant part of a long-term total return. In fact, if you include the compounding impact of dividends in the aforementioned S&P 500 return, your initial investment would have actually grown more than eightyfold! [v] Income matters.

Clearly, gold will exhibit periods of outperformance versus stocks, as has been the case so far in 2020. The same goes for many other assets: bitcoin, timber, or even tulips. But the bottom line is that gold is a trade to rent or an asset to wear. Stocks have proven to be a far more reliable hedge when they are given the time they deserve as perpetual, cash flowing, investments.

©2020 First Command Financial Services, Inc. is the parent company of First Command Brokerage Services, Inc. (Member SIPC, FINRA), First Command Advisory Services, Inc., First Command Insurance Services, Inc. and First Command Bank. Securities products and brokerage services are provided by First Command Brokerage Services, Inc. a broker-dealer. Financial planning and investment advisory services are provided by First Command Advisory Services, Inc., an investment adviser. Insurance products and services are provided by First Command Insurance Services, Inc. Banking products and services are provided by First Command Bank (Member FDIC). Securities are not FDIC insured, have no bank guarantee and may lose value.

The information in this report was prepared by John Weitzer, Chief Investment Officer of First Command. Opinions represent First Command’s opinion as of the date of this report and are for general informational purposes only and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally. First Command does not undertake to advise you of any change in its opinions or the information contained in this report.

This report is not intended to be a client-specific suitability analysis or recommendation, an offer to participate in any investment, or a recommendation to buy, hold or sell securities. Do not use this report as the sole basis for investment decisions. Do not select an asset class or investment product based on performance alone. Consider all relevant information, including your existing portfolio, investment objectives, risk tolerance, liquidity needs and investment time horizon. Should you require investment advice, please consult with your financial advisor. Risk is inherent in the market. Past performance does not guarantee future results. Your investment may be worth more or less than its original cost. Your investment returns will be affected by investment expenses, fees, taxes and other costs.

Footnotes

[1] Harvey, Jan. “Gold as an inflation hedge? Well, sort off…” Thomson Reuters. March 1, 2018.

[2] Elmerraji, Jonas. “Does Gold Work in a Stock Market Crisis?” The Street, Inc. July 27, 2020.

[3] Per Bloomberg: The Bloomberg US Dollar Index tracks the performance of a basket of ten leading global currencies versus the U.S. Dollar. Each currency in the basket and their weight is determined annually based on their share of international trade and FX liquidity.

[4] General analysis in first three bullet points sourced from: Murray, Nick. “The mind-numbing stupidity of gold.” Nick Murray Interactive. August 2020.

[5] Based a total compound annual return from Bloomberg using the COMP function and the S&P 500 Index

Get Squared Away®

Let’s start with your financial plan.

Answer just a few simple questions and — If we determine that you can benefit from working with us — we’ll put you in touch with a First Command Advisor to create your personalized financial plan. There’s no obligation, and no cost for active duty military service members and their immediate families.