The Path Forward

By: John S. Weitzer, CFA

Chief Investment Officer

Apr 13, 2020 | 10 min. read

Between February 19th and March 23rd, the S&P 500 stock index declined by approximately 35%[1]. Though it has since rallied, recouping approximately half of its losses, it now seems inevitable that this rapid market correction and the damage that has been done to our economy will lead to a somewhat unconventional recession here in the United States. Recessions typically occur in response to excesses built up during a business expansion. And harbingers of recessions are typically things like high inflation, high interest rates, overheating economic growth, bad or excessive debt, restrictive lending practices by banks or the popping of an asset bubble. Market corrections, on the other hand, tend to occur when investors become convinced that a business expansion is in its late stages or ending and that a recession may be coming.

How Did We Get Here?

The pending recession is unique in that it will not be the result of the same types of excess that cause most recessions, but of the singular event that is the COVID-19 outbreak and all the subsequent steps being taken to end it. In this sense, it will effectively be a self-administered recession. Let me illustrate.

- Coronavirus (or COVID-19) outbreak. This new virus originated in China in December of 2019[2] and has now spread worldwide. We did not have any experience with this specific pathogen.

- Pandemic models. An initial set of models were created by leading epidemiologists.[3] These models were created to provide governments with estimates to inform public policy responses to a potential pandemic. With little experience or data on this virus, these models predicted very dire outcomes if nothing was done to mitigate the spread of the infection. For instance, the pandemic model designed by Neil Ferguson from the Imperial College of London predicted 510,000 deaths in the United Kingdom and over 2.2 million deaths in the United States.[4] These model estimates were published in a report by the Imperial College COVID-19 Response Team on March 16, 2020.

- Government response. Governments around the world responded to these pandemic model estimates (which were eye-catching big numbers) with severe mitigation strategies such as travel bans, community quarantines, work from home policies, no large social gatherings, social distancing, and the list goes on.[5]

- Crisis of confidence. Governments’ severe response to this virus resulted in a crisis of confidence in the financial markets as the economic impact of these measures became clear.

- Market correction. This crisis of confidence predictably led to a “flight to safety” by investors and the sharp correction in markets around the world that we have witnessed.

- Recession. The upcoming recession will be not just the result of the pandemic, but of the severe mitigation strategies that were necessary to effectively reduce the human interaction associated with economic activity. Well regarded economist Jim Paulsen calls this recession an “artificial recession,” as it is the first self-administered recession in U.S. history.[6] Effectively, we have agreed to take our economic engine off-line for whatever time period is necessary to slow down the spread of this virus. Slowing down the spread prevents medical systems from being overwhelmed in order to minimize deaths.

As this chain of events demonstrates, our current situation is the direct result of the COVID-19 pandemic and the global response to it. The capital markets (stocks and bonds) intensely dislike uncertainty and we have been existing for weeks now in what feels like one of the most uncertain times in modern world history. The good news is that every day we learn more about this virus. As a result, each day that passes diminishes, by some degree, the level of uncertainty. Think of it as a large swimming pool with murky water that we are draining a little bit every day. Soon, we will be able to see the bottom and find the truth of the matter so that we can develop effective, appropriate responses to this virus.

The Path Forward

I see the path forward as a retracing of the steps we’ve taken to get here. Let’s look at them again, but with an eye towards what we have learned in the weeks since this challenging period began.

- Coronavirus (or COVID-19). What has been our experience with this new virus since it hit the world stage? Examining the infection path of this disease in multiple countries reveals that the infection period (or range) of the virus lasts for 8-10 weeks and includes an ascent phase (increasing daily infection cases), a peak (levelling off of daily infection cases), and a descent (decreasing daily infection cases).[7] Once this descent begins and those recovered increase, the active case load of infections goes down. China, South Korea, Italy, Spain and Germany have arguably moved into the descent phase. We have learned that the original Case Fatality Rates (or CFRs) are lower than predicted. The World Health Organization (WHO) originally stated that the CFR rate was around 3.4%. That number now appears to be settling closer to 1%.

- Pandemic models. As we learn more about this virus, the new information being input into the pandemic models is changing the output estimates. Now, Neil Ferguson is predicting that there will be less than 20,000 deaths in the United Kingdom as compared to his original estimate of 510,000 deaths. That is a 96% reduction in the death estimate.[8] The official United States death estimate is now 100,000 to 240,000, instead of 2.2 million.[9] The pandemic model from the Institute for Health Metrics and Evaluation (IHME), which is backed by the Gates Foundation, is now forecasting 60,000 U.S. deaths.[10]

- Government response to pandemic models. Based on new estimates from the pandemic models, governments that initially responded with severe mitigation strategies may begin moderating their mitigation strategies to strike a balance between protecting those that are most vulnerable to this virus (those older than 60 years of age and those with complicating health factors such as respiratory illnesses, diabetes, heart disease, obesity, etc.) while allowing others in low-risk categories (those under 60 who are healthy and those that have recovered from the virus) to get back to work.

- Crisis of confidence. Reduced pandemic model estimates and moderating government responses should begin to reduce the public’s anxiety and the crisis of confidence among investors.

- Market correction. As public fears begin to recede and investors begin to see a light at the end of the tunnel, capital markets should begin recovering. This reversal could be sharp (a v-shaped recovery) or prolonged. It’s too early to tell how quickly an economic recovery can be engineered.

- Recession. We will be left with the recession and its depth and magnitude will be dependent on how quickly the previous steps take place. The longer severe mitigation strategies are deemed necessary, the longer the economic recovery will take. Chief Economist Brian Wesbury states that the “longer these measures persist, the greater the risk of atrophy setting in for small business across the country, making them less able to reopen in the future. The loss of intangible capital would be enormous, the internal knowledge of how to get things done. Slower economic growth in the post-COVID19 world would be the result.”[11]

The Recession and Unemployment

We now have a recession on our hands. How bad will it be? IHS Markit, London-based global information provider, estimates that the U.S. economy will shrink 5.4% in 2020.[12] This would be a deeper recession than the one in 2008-2009, which was -2.5%. Goldman Sachs is predicting a contraction of 3.1%.[13] Most of the estimates seem to show a deep decline in the 2nd quarter of 2020, a less severe decline in the 3rd quarter, followed by a positive number in the 4th quarter. The unemployment rate, which started the year at 3.5%, is now 4.4%.[14] If 20 to 25 million people lose their jobs in the next two months, the unemployment rate could climb as high as 16%.[15] Compare that number with the high-water mark of 9% unemployment during the 2008-2009 recession. The Asian Development Bank predicts that the world’s economic output will drop by 5%, or $4 Trillion. These are extremely ugly numbers.

Keep in mind, though, that the equity markets are a forward-predicting device. These bad numbers may already be baked into current stock prices. We have known for a couple of weeks that we were heading into a recession and the unemployment rate numbers were going to be extremely bad. For instance, on March 26th, the initial claims report (those filing for unemployment) came in at 3.3 million. On that same day, the S&P 500 went up 129 points. Then, on April 2nd, the initial claims report showed 6.6 million – a truly shocking number - filing for unemployment. And yet, on that same day, the S&P 500 went up 69 points. Again, on April 9th, the initial claims report showed 6.6 million. The market was up 40 points for the day. During the 2008-2009 Great Financial Crisis, the initial unemployment claims report never rose over 700,000. My best guess at this point is that the recession will be deep and severe, and as mentioned above, the question of how long it will last will ultimately depend on how soon we are able to overcome the virus and get people back to work.

Positive Points

When things get cloudy, I tend to look for silver linings. Here are several for your consideration.

- To bridge the economic output gap caused by our affirmative decision to implement severe mitigation strategies, government policymakers have reacted to the economic damage with massive fiscal and monetary accommodation measures.[16]

- The Federal Reserve has reduced interest rates to nearly zero, restarted quantitative easing (increasing the U.S. money supply), and is now backstopping an unprecedented array of markets, including commercial paper, money markets, commercial mortgages, and municipal securities.[17]

- Meanwhile, we have a newly enacted stimulus bill that totals over $2 trillion. It includes IRS checks, an expansion in unemployment benefits, grants, loans, and loan guarantees for businesses (large and small), hospitals, schools, companies in which the U.S. government has a national security interest (energy companies), and state and local governments.[18]

- We have had a long period of low unemployment and the U.S. household personal saving rate stood at 8% at the end of 2019.[19] Compare this “rainy day savings” with prior to the 2001 recession (<5%) and the 2008 recession (<4%).[20] This data shows that many U.S. households built up a buffer by accumulating savings during the last business expansion.

- The household debt-service burden is at a record low of 9.7% compared to a 12.4% debt burden at the start of the 2001 recession, and 13.2% in 2008.[21] Many households kept their debt level very low prior to this recession.

- U.S. corporations appeared to be in very solid shape entering this recession. U.S. companies have an uncommonly high level of liquidity and have not abused debt as they often did in prior business expansions.[22]

- The quickness and severity of this recession was caused by a decision to suspend our economy (we shut it down). How quickly would the economy come back if we decided to go back to work? Jim Paulsen states that “should the virus curve show a bend in the next couple of months, the recovery in both the economy and the stock market could prove much sharper and faster than many appreciate.”[23]

China's Experience

China was the first country to deal with the coronavirus (COVID-19), as it was the epicenter of the outbreak. They went through the curve (ascent, peak, descent) of active cases. The economic data coming out of China is the worst seen in modern times.[24] From January to February, year over year, retail sales were down 20%, exports were down 17%, fixed asset investments were down 25%, and industrial production was down 13%.[25] Franklin Templeton predicts that China will experience a sharp rebound of economic activity over the 2nd half of 2020, “driven by pent up demand and government stimulus”.[26]

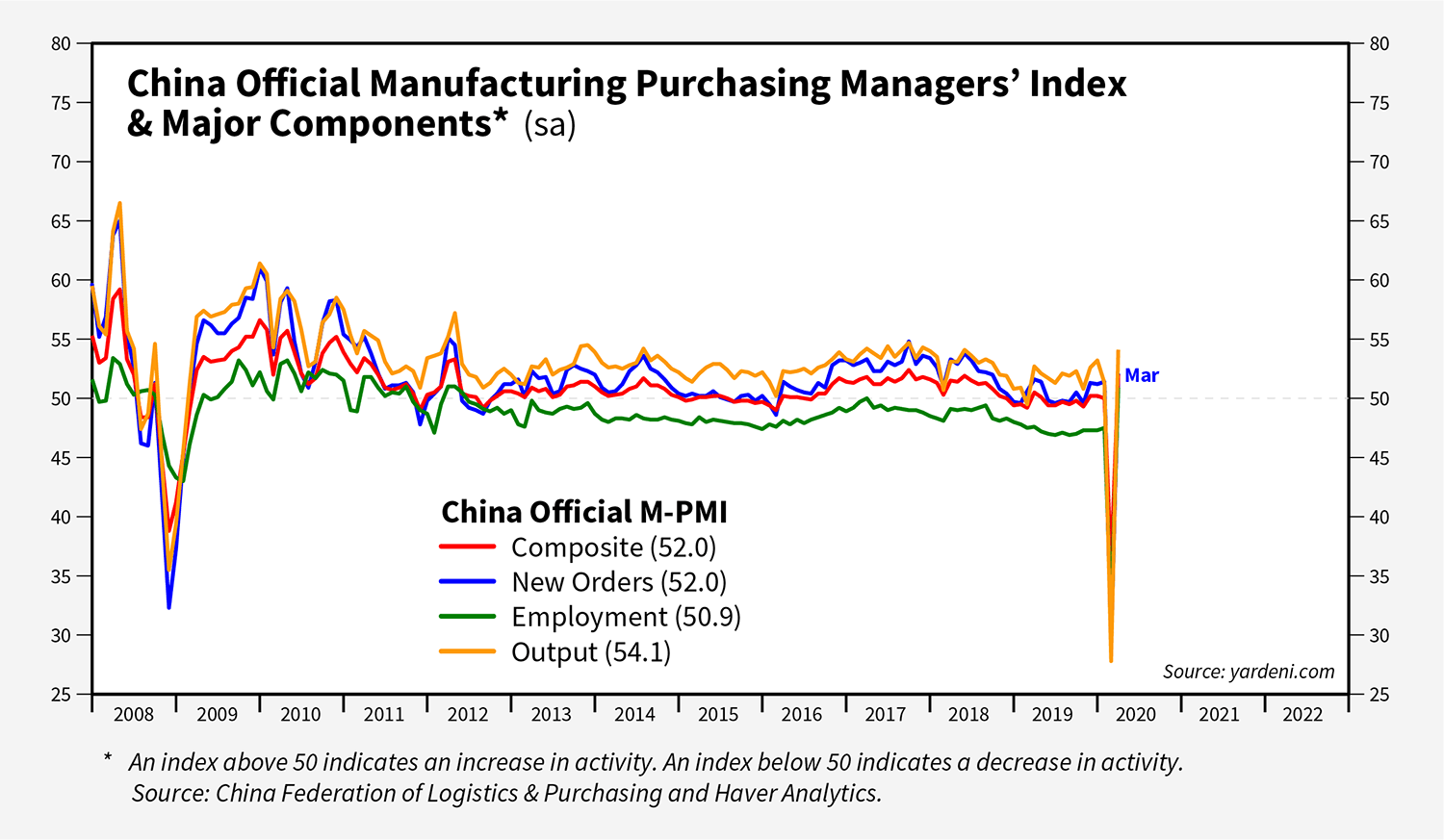

China is an example of an economic snapback once the population can get back to work. Let’s review the chart below.[27] This index tracks the manufacturing output of China (yellow line). An index reading under 50 indicates that the manufacturing output is contracting. As you can see below, this manufacturing activity declined sharply in February. The index also sharply recovered in March once their workers could go back to work. Once China lifted its severe mitigation strategies (an active decision to turn the economy back on), the country’s economic activity quickly came back.

Summary

We have had a sharp stock market correction. We now will have a recession. Our path forward is a retracing of the steps we’ve taken to get here. The length of our recession is likely to depend on when we can get the U.S. economic engine humming again. Doing so, of course, requires overcoming the virus so that we can moderate the current mitigation strategies and, ultimately, put the country back to work. If we can accomplish that soon, we most likely will have the same experience as China – an economic output snapback.

We will continue to closely monitor and keep you apprised of developments related to the COVID-19 pandemic that could affect the economy or markets. Even in the midst of the frantic activity we have seen and will likely continue to see in financial markets, we remain steadfast in our belief that a well-designed, globally diversified portfolio that is aligned with your financial plan, investment time horizon and risk comfort level is the best strategy for weathering the current storm and pursuing your long-term goals when the pandemic recedes. If you have questions or concerns specific to your situation that have not been addressed, please do not hesitate to reach out to your Advisor. Thank you for the confidence you have placed in First Command.

The information in this report was prepared by John Weitzer, Chief Investment Officer of First Command. Opinions represent First Command’s opinion as of the date of this report and are for general informational purposes only and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally. First Command does not undertake to advise you of any change in its opinions or the information contained in this report. This report is not intended to be a client-specific suitability analysis or recommendation, an offer to participate in any investment, or a recommendation to buy, hold or sell securities. Do not use this report as the sole basis for investment decisions. Do not select an asset class or investment product based on performance alone. Consider all relevant information, including your existing portfolio, investment objectives, risk tolerance, liquidity needs and investment time horizon. Should you require investment advice, please consult with your financial advisor. Risk is inherent in the market. Past performance does not guarantee future results. Your investment may be worth more or less than its original cost. Your investment returns will be affected by investment expenses, fees, taxes and other costs.

All estimates provided are for informational purposes only and should not be relied on to make investment or other decisions. Should you require investment advice, please consult with your financial advisor. Risk is inherent in the market. Past performance does not guarantee future results. Your investment may be worth more or less than its original cost. Your investment returns will be affected by investment expenses, fees, taxes and other costs.

The S&P 500 Index is widely regarded as the best single gauge of the U.S. equities market. This world-renowned index includes a representative sample of 500 leading companies in leading industries of the U.S. economy. Although the S&P 500 Index focuses on the large-cap segment of the market, with approximately 75% coverage of U.S. equities, it is also an ideal proxy for the total market. An investor cannot invest directly in an index.

©2020 First Command Financial Services, Inc. parent of First Command Financial Planning, Inc. (Member SIPC, FINRA), First Command Advisory Services, Inc., First Command Insurance Services, Inc. and First Command Bank. Securities and brokerage services are offered by First Command Financial Planning, Inc., a broker-dealer. Financial planning and investment advisory services are offered by First Command Advisory Services, Inc., an investment adviser. Insurance products and services are offered by First Command Insurance Services, Inc. Banking products and services are offered by First Command Bank. Securities products are not FDIC insured, have no bank guarantee and may lose value. A financial plan, by itself, cannot assure that retirement or other financial goals will be met. In Europe, investment and insurance products and services are offered through First Command Europe Limited. First Command Europe Limited is a wholly owned subsidiary of First Command Financial Services, Inc. and is authorized and regulated by the Financial Conduct Authority. Certain products and services offered in the United States may not be available through First Command Europe Limited.

Footnotes

[1] The high on the S&P 500 was 3,393 on 2/19/20. The lowest point so far in this correction was on 3/23/20 when the index hit 2,191 (down -35%).

[2] There is evidence to suggest that China was aware of this earlier than December and that they have not been reporting the truth of their experience with the disease.

[3] Epidemiology is the study of the distribution and determinants of health-related states or events in specified populations, and the application of this study to the control of health problems (https://www.cdc.gov/training/publichealth101/epidemiology.html).

[5] https://www.nytimes.com/2020/03/17/world/europe/coronavirus-imperial-college-johnson.html.

[6] “A Recession Without a Purpose?” by James Paulsen, Leuthold Group (March 31, 2020).

[7] A good source of information on the spread of this virus can be found on the Worldometer websites (https://www.worldometers.info/coronavirus/). You can examine the infection globally and by country.

[9] https://www.nytimes.com/2020/03/31/us/politics/coronavirus-death-toll-united-states.html.

[10] https://covid19.healthdata.org/projections.

[11] Monday Morning Outlook – The Coronavirus Threat by Brian Wesbury of First Trust (March 30, 2020).

[13] Same.

[15] Same.

[16] Monday Morning Outlook – The Coronavirus Threat by Brian Wesbury of First Trust (March 30, 2020).

[17] Same.

[18] Same.

[19] “A Recession Without a Purpose?” by James Paulsen, Leuthold Group (March 31, 2020).

[20] Same.

[21] Same.

[22] Same.

[23] Same.

[24] “China: Coming out of COVID-19” by Manraj Sekhon, CFA, Chief Investment Officer, Franklin Templeton Emerging Markets Equity (Page 5 of “The path to recovery: What’s next? – Franklin Templeton Thinks, Global Investment Outlook”) (April 2020).

[25] Same.

[26] Same (Page 5-6).

[27] “Country Briefing: China” by Yardeni Research, Inc. (March 31, 2020).

Get Squared Away®

Let’s start with your financial plan.

Answer just a few simple questions and — If we determine that you can benefit from working with us — we’ll put you in touch with a First Command Advisor to create your personalized financial plan. There’s no obligation, and no cost for active duty military service members and their immediate families.